What Does the HMRC Letter Look Like?

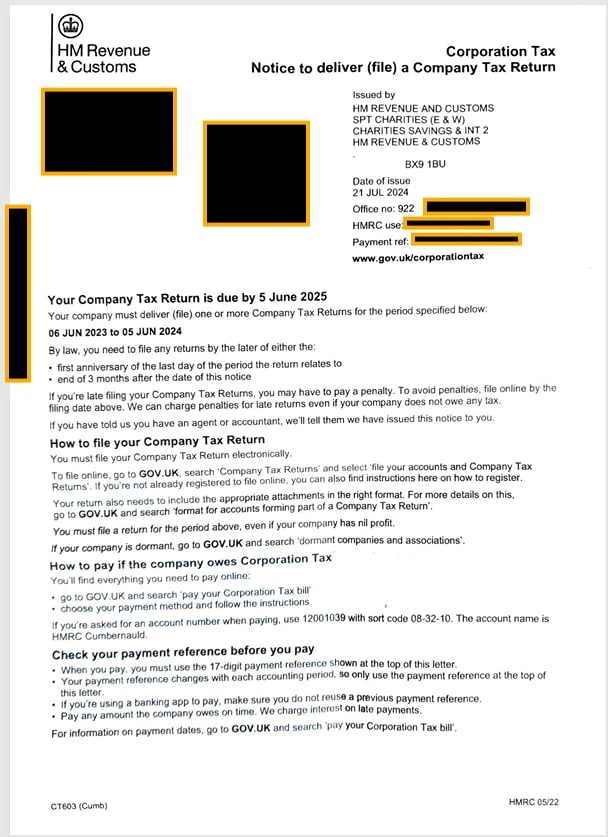

When HMRC sends a Corporation Tax notice to a charity, you will receive a letter titled "Corporation Tax Notice to Deliver a Corporation Tax Return" (commonly known as a CT603 notice). This official document requests your charity to file a CT600 Corporation Tax return by a specific deadline.

Example of an HMRC Corporation Tax notice showing the filing deadline

Important: The letter will clearly state the filing deadline. Missing this deadline can result in penalties even if no Corporation Tax is due.