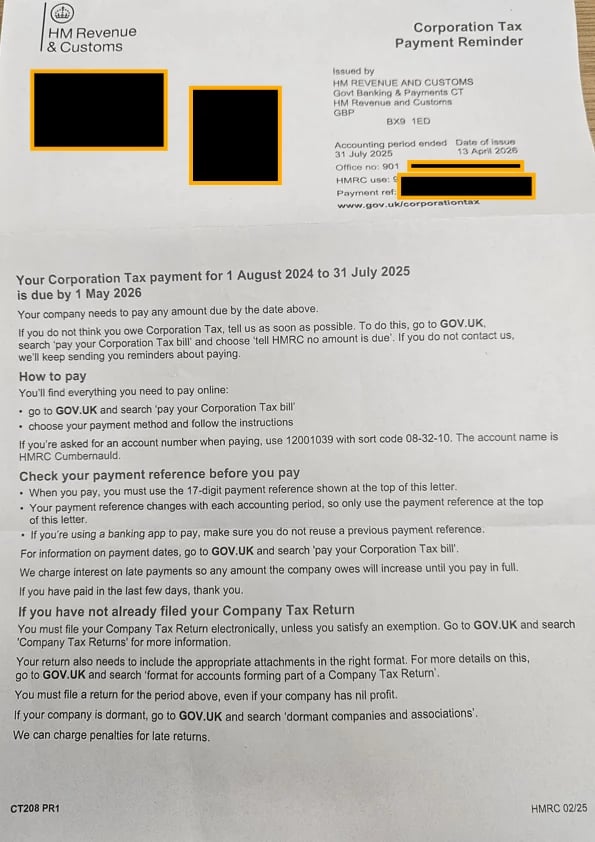

What Does the HMRC Letter Look Like?

The HMRC Corporation Tax Payment Reminder letter is an official document from HM Revenue and Customs regarding Corporation Tax for a specific tax period. Below is an example of what this letter looks like.

Example of an HMRC Corporation Tax Payment Reminder letter for charities

Important: Receiving this letter does not automatically mean your charity owes Corporation Tax. However, it should never be ignored.